Chemicals and Plastics - Global Outlook January 2021

The year 2020 witnessed a global Covid pandemic and the biggest GDP reduction since the Great Depression of 1929. Of course, Chemicals & Plastics (C&P) have also been affected globally, but there is no public data available yet for the year.

We will take a look at 2019 and 2024. Most experts are saying that 2021 will be a recovery year, and the International Monetary Fund (IMF) has made GDP forecasts by region.

In this article I will share global market data for C&P with regional details for installed capacity and operating rates, along with current (2019) and future (2024) demand and growth rates. The demand forecast presented here is aligned with the IMF data. You can also download the full article here: ![]() Chemicals_Plastics_-_Global_Outlook_2020.pdf

Chemicals_Plastics_-_Global_Outlook_2020.pdf

This aggregated market analysis was executed on 147 C&P products totaling 3.6 billion MT (7.8 trillion lb.) of global products. These products represent US$2.5 trillion of revenue in 2019. According to Statista, this represents 44% of the global chemical industry, in other words, a good representation of total production.

Background

There are thousands of chemical products on the market. However, the data from this market analysis are restricted to chemicals most consumed in the industry (solid, liquid, or gas) considered as commodity chemicals. They include Caustic Soda, Ethylene, Propylene, Methanol, Sulfuric Acid, among others.

The term Plastics is very broad, and each reader will naturally relate to a different product. Here, I include as a Plastic any polymer (large molecule composed of repeated subunits), thermoplastic or thermoset, elastomer, rubber, copolymer, or resin in any form (pellet, powder, liquid, etc.). Plastics products include Polyethylene (LDPE, LLDPE, HDPE), PET, PP, PVC, Amino resins, Natural Rubber, PS, ABS, PC, PVA, Epoxy, Silicone, and Acrylics.

In terms of regions, the data was aggregated as North America (USA, Canada, Mexico), Latin America (Central, South), Europe (Western, Eastern, Central, Baltic), Middle East & Africa, and Asia-Pacific (India, Southeast, Northeast, Oceania).

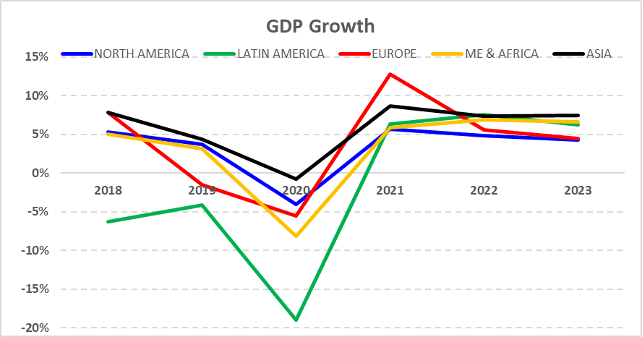

Global Economy

It is important to point out that all regions had negative GDP growth in 2020. The IMF publishes twice-yearly historical reports and forecasts of GDP for 195 countries. I have aggregated the data from the latest publication (Oct. 2020) by region as shown below.

It appears that experts’ predictions of 2021 as the recovery year is aligned with IMF forecasts.

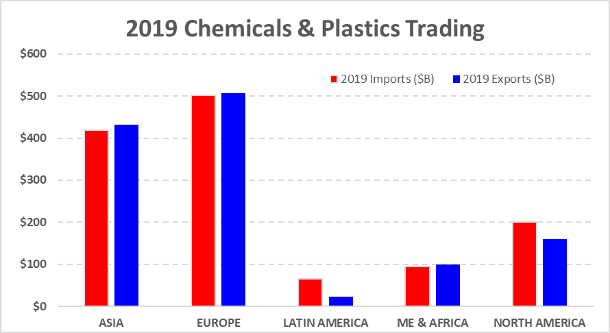

Trading Data

According to Trade Map, around US$ 1.2B of C&P (30% of total revenue) was traded between countries. I have aggregated this data by region as shown below.

The data shows North and Latin America to be net buyers, while Europe, Asia, and MEA are net sellers.

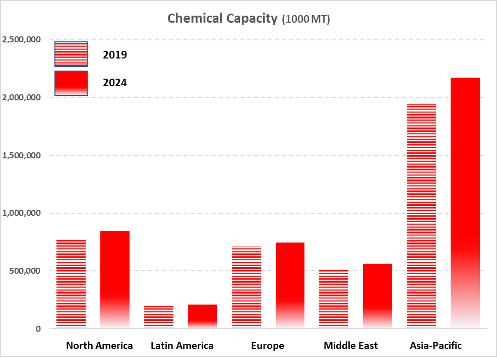

Capacity

The global 2019 capacity for all Chemicals was around 4.2 billion MT (2.5% higher than 2018), where Asia-Pacific represented the highest capacity (47%) among regions shown in Chart I. The global capacity for all Plastics families was around 457 million MT (2.6% higher than 2018), where Asia-Pacific again represented the highest capacity (59%) of all regions together as shown below. Note especially the difference in the scale of magnitude.

Chart 1

As seen above, the Asia-Pacific installed capacity in Chemicals (47%) was followed by North America (19%), Europe (17%), the Middle East (12%), and Latin America (5%). In Plastics, Asia-Pacific’s installed capacity (59%) was followed by North America (15%), Europe (14%), the Middle East (8%), and Latin America (3%).

The high capacity, of course, means a high market demand in the region, but it also represents an alternative for purchasing officers to import from that region.

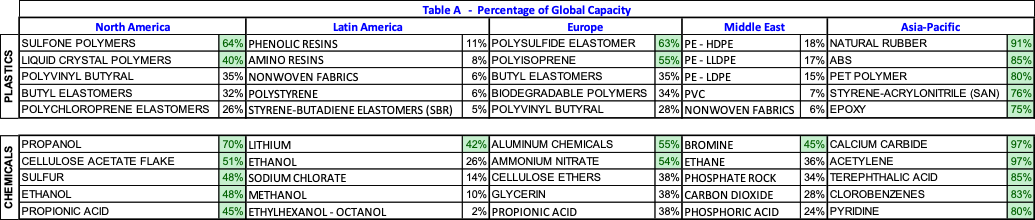

Some C&P capacities show higher concentrations in specific regions. Table A below shows, by region, which C&P have the highest concentrations of capacity (local capacity/global capacity). Having a higher capacity concentration may mean that the region has an abundance of – and likely lower costs for – that specific feedstock. It could also mean lower total unit fixed costs (manufacturing and expenses) because of higher production volumes. Consumers of these products should consider sourcing from these regions. The green cells in the table highlight dominance on a global basis.

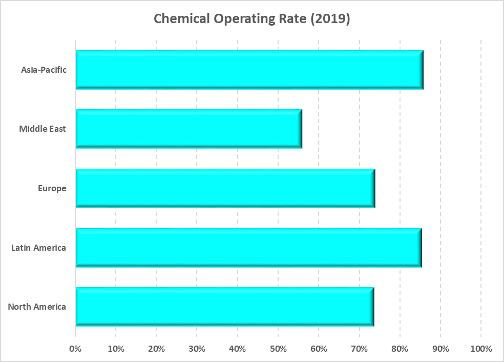

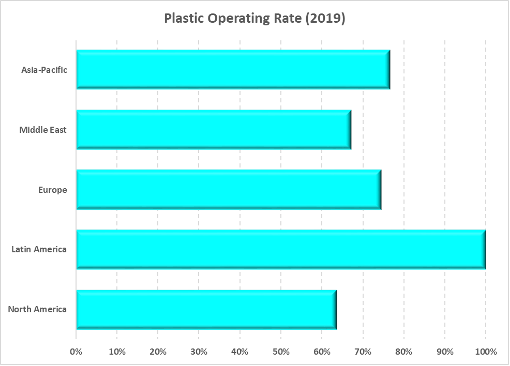

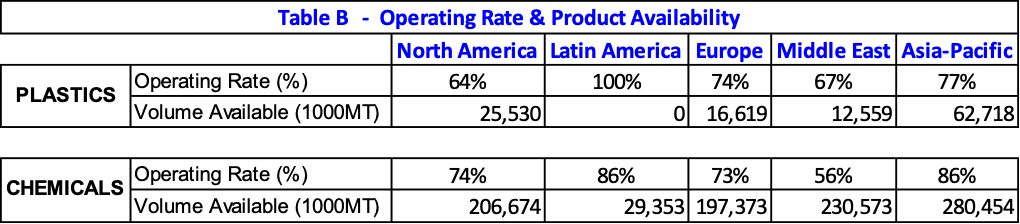

Operating Rates

Chart 2 below shows the aggregated operation rates for Chemicals and Plastics in each region as of 2019.

Chart 2

The analysis of operation rates can be considered from two perspectives: Unit Cost and Product Availability.

Higher percentage represents lower unit fixed costs (in manufacturing and expenses) compared to the other regions on the same basis. Basically, this is because we divide all fixed costs and expenses by a higher volume of produced products. However, each C&P family presents a different impact of fixed costs on the total cost, as well as the magnitude of fixed costs from different sizes of production plants. For example, with Cumene, the unit fixed cost can be 5% to 7% (highest to lowest capacity) and with Sulfuric Acid, 61% to 75%. For Polystyrene, the unit fixed cost can be 10% to 16% (highest to lowest capacity) and with LLDPE, 33% to 42%.

The second perspective is to see where there may be more products available to buy from. In this calculation, we need to consider the operating rates and installed capacities together. Table B shows both data sets by region.

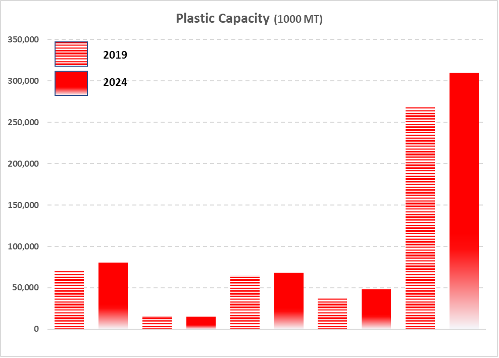

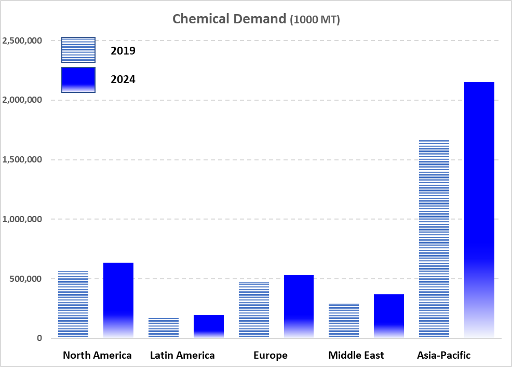

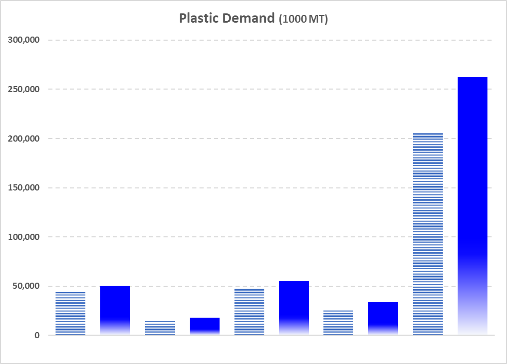

Demand

Chart 3 shows the aggregated demand for Chemicals and Plastics in each region in 2019 and estimated for 2024.

Chart 3

The graphs above look very similar, but the scales are 10-fold different. For Chemicals & Plastics, Asia-Pacific represents the highest demand in 2019 as well as for the future, followed by North America, Europe, the Middle East, and Latin America. This picture follows the same pattern as shown in Chart 1 – Capacity.

Nine Plastics represent 85% of global demand: PET, HDPE, PVC, LLDPE, LDPE, Amino Resins, Natural Rubber, Polystyrene, Nonwoven Fabric, and ABS. In Chemicals, ten products represent 49% of global demand: Sodium Chloride, Sulfuric Acid, Ammonia, Ethylene, Propylene, Ethanol, Urea, Sulfur, Methanol, and Caustic Soda.

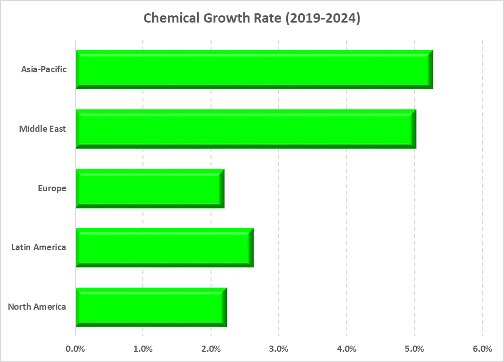

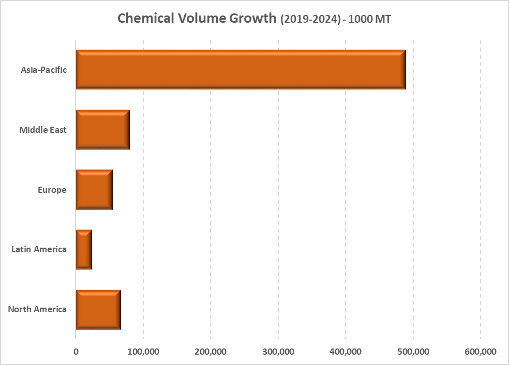

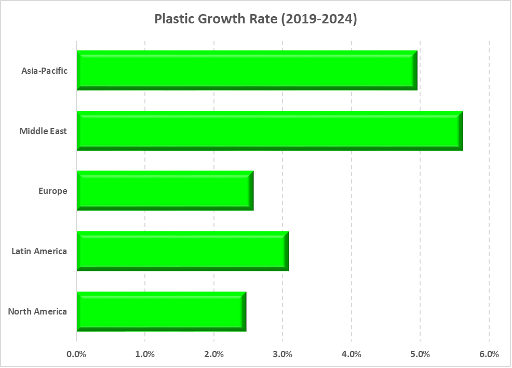

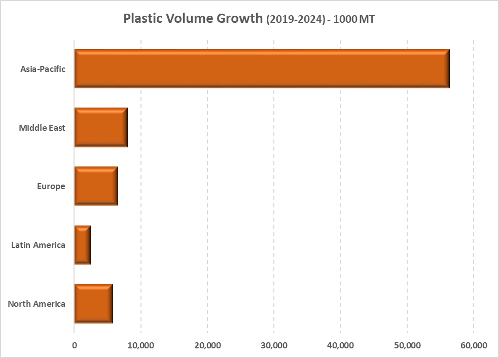

Volume Growth & Growth Rates

The Compound Average Growth Rate (CAGR) is the growth rate in percentage year over year for a specific region. It reflects the growth of all end-use applications of that specific C&P in a region; besides specific drivers, it is driven by the overall growth of the region’s GDP and GDP/Capita.

Chart 4 shows the regional growth rate (CAGR) and Volume Growth for Chemicals, with Chart 5 showing the same for Plastics. As evident for Chemicals, the biggest growth will be in Asia, in terms of both percentage and volume, aligned with the biggest demand and capacity. For Plastics, the biggest growth will be in the Middle East, but in terms of volume, Asia is leading.

Chart 4

Chart 5

The biggest growth areas in Chemicals will be Rare Earth Minerals (9.7%), Lactic Acid (9.6%), Methanol (7.4%), Activated Carbon (7%), and Lithium (6.4%). Growth in Plastics will be in Biodegradable Polymers (11.5%), Liquid Crystal Polymers (6.0%), Acrylic Resins (5.9%), Polyvinyl Butyral (5.6%), and Silicone (5.6%).

Conclusion

2020 was a terrible year, both for people and for businesses. As the above numbers show, Chemicals & Plastics will recover in 2021. C&P are used across all manufacturing industries as first- or second-tier materials, so it is important to understand market dynamics in the C&P world. From the business perspective, it is imperative to understand the supply and demand of each C&P family and the competitive position in each region in order to define long-term business strategy. From the purchasing perspective, managers need to educate themselves at a granular level on each C&P family they buy, so they can select the suppliers that best fit long-term needs, in addition to identifying opportunity for lower-cost materials.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.